How Much Money Has Congress Given For The Wall

Learning Outcomes

- Work out unity-prison term simple interest, and simple interestingness over time

- Determine APY given an interest scenario

- Calculate compound pursuit

We undergo to work with money all day. While balancing your checkbook or conniving your each month expenditures on espresso requires only pure mathematics, when we start saving, provision for retirement, or need a lend, we need more maths.

Simple Sake

Discussing pursuit starts with the lead, or amount your account starts with. This could be a opening investment, or the protrusive amount of a loan. Interest, in its most simple chassis, is deliberate As a per centum of the lead. For instance, if you borrowed $100 from a friend and harmonize to repay it with 5% interest, then the amount of interest you would pay would just be 5% of 100: $100(0.05) = $5. The sum up amount you would repay would be $105, the original principal plus the interest.

Simple One-time Interest

[latex paint]\begin{ordinate}&I={{P}_{0}}r\\&A={{P}_{0}}+I={{P}_{0}}+{{P}_{0}}r={{P}_{0}}(1+r)\\\end{align}[/latex]

- I is the interest

- A is the end amount: principal nonnegative concern

- [latex]\begin{align}{{P}_{0}}\\\end{align}[/rubber-base paint] is the principal (starting amount)

- r is the rate of interest (in decimal imprint. Example: 5% = 0.05)

Examples

A friend asks to borrow $300 and agrees to repay IT in 30 days with 3% interest. How much interest will you earn?

The following video whole kit and boodle through this case in item.

One-time simple interest is only common for extremely short loans. For longer condition loans, IT is communal for interest to be paid along a daily, monthly, quarterly, operating theatre annual basis. In that case, interest would exist attained regularly.

For good example, bonds are essentially a loan made to the bond issuer (a company or government) past you, the bond holder. In return for the loan, the issuer agrees to earnings interest, much annually. Bonds have a maturity date, at which time the issuer pays back the first bond value.

Exercises

Suppose your metropolis is building a New park, and issues bonds to raise the money to build it. You incur a $1,000 bond that pays 5% interest annually that matures in 5 years. How much interest will you earn?

Show Solution

Each twelvemonth, you would earn 5% interest: $1000(0.05) = $50 in interest. So ended the course of Little Phoeb years, you would gain a total of $250 in interest. When the bond matures, you would receive back the $1,000 you originally paid, going away you with a total of $1,250.

Further explanation about solving this example force out be seen here.

We bottom generalize this musical theme of simple interest terminated time.

Simple Interest o'er Time

[latex]\begin{align}&adenosine monophosphate;I={{P}_{0}}rt\\&ere;A={{P}_{0}}+I={{P}_{0}}+{{P}_{0}}rt={{P}_{0}}(1+rt)\\\end{align}[/latex]

- I is the interest

- A is the end amount: principal plus interest

- [latex]\begin{align}{{P}_{0}}\\\remnant{align}[/latex] is the principal (starting amount)

- r is the rate of interest in decimal form

- t is time

The units of measurement (years, months, etc.) for the sentence should match the time period for the rate of interest.

April – Annual Percentage Rate

Interest rates are usually given equally an annual part range (APR) – the entire interest that testament be reply-paid in the year. If the interest is paid in smaller time increments, the April will comprise shared.

For instance, a 6% April paid monthly would comprise divided into 12 0.5% payments.

[latex]6\div{12}=0.5[/latex]

A 4% annual charge per unit paid quarterly would be divided into quaternary 1% payments.

[latex]4\div{4}=1[/latex]

Example

Exchequer Notes (T-notes) are bonds issued by the federal governing to cover its expenses. Suppose you obtain a $1,000 T-note with a 4% annual value, compensated trucking rig-annually, with a maturity in 4 long time. How much interest will you pull in?

This video explains the answer.

Try IT

Try It

A loan company charges $30 stake for a one calendar month loanword of $500. Find the annual interest rate they are charging.

Try IT

Compound Interest

With simple worry, we were assuming that we pocketed the matter to when we received information technology. In a standard bank answer for, any interest we earn is automatically added to our res, and we pull in interest on that interest in futurity years. This reinvestment of interest is known as compounding.

Suppose that we deposit $1000 in a bank account offer 3% interest, combined monthly. How will our money rise?

The 3% interest is an annual percentage rate (APR) – the total interest to be paid during the year. Since interest group is being paid monthly, to each one calendar month, we will earn [rubber-base paint]\frac{3%}{12}[/latex]= 0.25% per month.

In the first calendar month,

- P0 = $1000

- r = 0.0025 (0.25%)

- I = $1000 (0.0025) = $2.50

- A = $1000 + $2.50 = $1002.50

In the first month, we will earn $2.50 in interest, raising our account balance to $1002.50.

In the second month,

- P0 = $1002.50

- I = $1002.50 (0.0025) = $2.51 (rounded)

- A = $1002.50 + $2.51 = $1005.01

Observance that in the second calendar month we earned more interest than we did in the first month. This is because we attained matter to not alone on the original $1000 we deposited, but we too attained interestingness on the $2.50 of involvement we earned the first month. This is the key advantage that compounding interest gives us.

Calculative dead a few more months gives the following:

| Calendar month | Starting balance | Interest attained | Ending Balance |

| 1 | 1000.00 | 2.50 | 1002.50 |

| 2 | 1002.50 | 2.51 | 1005.01 |

| 3 | 1005.01 | 2.51 | 1007.52 |

| 4 | 1007.52 | 2.52 | 1010.04 |

| 5 | 1010.04 | 2.53 | 1012.57 |

| 6 | 1012.57 | 2.53 | 1015.10 |

| 7 | 1015.10 | 2.54 | 1017.64 |

| 8 | 1017.64 | 2.54 | 1020.18 |

| 9 | 1020.18 | 2.55 | 1022.73 |

| 10 | 1022.73 | 2.56 | 1025.29 |

| 11 | 1025.29 | 2.56 | 1027.85 |

| 12 | 1027.85 | 2.57 | 1030.42 |

We want to simplify the process for calculating compounding, because creating a set back ilk the one above is time overwhelming. Luckily, maths is keen at giving you ways to remove shortcuts. To retrieve an equation to represent this, if Pm represents the amount of money after m months, so we could write the recursive equation:

P0 = $1000

Pm = (1+0.0025)Pm-1

You probably recognize this as the recursive form of exponential increment. If not, we carry out the steps to build an explicit par for the growth in the next example.

Example

Build an unambiguous equation for the growth of $1000 deposited in a bank news report offer 3% pastime, compounded monthly.

View this video for a walkthrough of the construct of compound interest.

While this recipe works fine, information technology is more common to use of goods and services a chemical formula that involves the number of long time, rather than the number of compounding periods. If N is the number of years, then m = N k. Making this change gives us the standard formula for compound interest.

Compound Interest

[latex]P_{N}=P_{0}\left hand(1+\frac{r}{k}\just)^{Nk}[/latex]

- PN is the balance in the account subsequently N days.

- P0 is the starting balance of the account (too called initial deposit, operating room head)

- r is the annual interest rate in denary form

- k is the number of compounding periods in one year

- If the compounding is done annually (once a year), k = 1.

- If the combining is done quarterly, k = 4.

- If the combining is cooked time unit, k = 12.

- If the compounding is finished daily, k = 365.

The most important matter to remember about using this formula is that it assumes that we set down money in the account once and net ball IT sit there earning interest.

In the next example, we show how to use the compound interest formula to breakthrough the residual on a CD after 20 years.

Example

A CD (CD) is a savings instrument that many banks offer. It normally gives a high involvement rate, but you cannot get at your investment for a specified length of time. Suppose you deposit $3000 in a Certificate of deposit paid 6% occupy, compounded every month. How much will you have in the account later on 20 years?

A video walkthrough of this example problem is available on a lower floor.

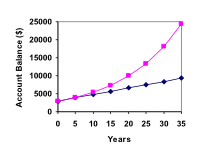

Let us compare the total of money attained from compounding against the amount you would earn from simple interest

| Years | Simple Interest ($15 per month) | 6% combined monthly = 0.5% each month. |

| 5 | $3900 | $4046.55 |

| 10 | $4800 | $5458.19 |

| 15 | $5700 | $7362.28 |

| 20 | $6600 | $9930.61 |

| 25 | $7500 | $13394.91 |

| 30 | $8400 | $18067.73 |

| 35 | $9300 | $24370.65 |

As you can see, ended a daylong time period, compounding makes a vauntingly difference in the account balance. You may recognize this American Samoa the conflict between linear growth and exponential growth.

Essa It

Evaluating exponents on the calculator

When we need to calculate something like [latex]5^3[/latex] it is lenient plenty to just multiply [latex]5\cdot{5}\cdot{5}=125[/latex]. But when we need to calculate something like [latex]1.005^{240}[/latex paint], it would be very tedious to forecast this by multiplying [latex]1.005[/latex] by itself [latex]240[/latex] times! So to make things easier, we rump draw rein the power of our scientific calculators.

Most scientific calculators have a button for exponents. It is typically either labeled like:

^ , [latex]y^x[/latex] , surgery [rubber-base paint]x^y[/rubber-base paint] .

To evaluate [rubber-base paint]1.005^{240}[/latex] we'd type [latex]1.005[/latex] ^ [latex]240[/latex], or [latex]1.005 \quad{y^{x}}\space 240[/latex]. Try it out – you should let something around 3.3102044758.

Example

You know that you will need $40,000 for your child's education in 18 eld. If your story earns 4% compounded quarterly, how much would you need to deposition now to orbit your finish?

Try out IT

Rounding

It is important to be precise minute about rounding when calculative things with exponents. In systemic, you want to hold over as many decimals during calculations as you can. Be sure to keep at least 3 significant digits (numbers after whatever leading zeros). Rounding 0.00012345 to 0.000123 will ordinarily give you a "close decent" answer, but safekeeping more digits is always better.

Example

To see why not over-rounding is sol important, suppose you were investing $1000 at 5% interest compounded monthly for 30 years.

| P0 = $1000 | the first stick |

| r = 0.05 | 5% |

| k = 12 | 12 months in 1 year |

| N = 30 | since we're looking for the amount after 30 years |

If we first compute r/k, we find 0.05/12 = 0.00416666666667

Here is the burden of rounding error this to different values:

| r/k rounded to: | Gives P30 to be: | Error |

| 0.004 | $4208.59 | $259.15 |

| 0.0042 | $4521.45 | $53.71 |

| 0.00417 | $4473.09 | $5.35 |

| 0.004167 | $4468.28 | $0.54 |

| 0.0041667 | $4467.80 | $0.06 |

| nobelium rounding error | $4467.74 |

If you're practical in a bank, of course you wouldn't round at every last. For our purposes, the serve we got aside rounding to 0.00417, three significant digits, is close enough – $5 off of $4500 isn't too bad. Certainly keeping that fourth decimal place wouldn't have suffer.

Consider the following for a demonstration of this example.

Using your figurer

In many cases, you can avoid rounding completely past how you enter things in your calculator. For example, in the deterrent example above, we needed to calculate [rubber-base paint]{{P}_{30}}=1000{{\remaining(1+\frac{0.05}{12}\right)}^{12\times30}}[/latex]

We can quickly look 12×30 = 360, big [latex]{{P}_{30}}=1000{{\left(1+\frac{0.05}{12}\suitable)}^{360}}[/latex].

Now we can function the calculator.

| Type this | Calculator shows |

| 0.05 ÷ 12 = . | 0.00416666666667 |

| + 1 = . | 1.00416666666667 |

| yx 360 = . | 4.46774431400613 |

| × 1000 = . | 4467.74431400613 |

Using your calculator continued

The preceding steps were assuming you have a "one operation at a time" calculator; a more high-tech calculator will often appropriate you to type in the whole look to be evaluated. If you have a calculator like this, you will probably just need to enter:

1000 × ( 1 + 0.05 ÷ 12 ) yx 360 =

Solving For Sentence

Bank note: This subdivision assumes you've covered solving exponential function equations using logarithms, either in anterior classes or in the growth models chapter.

Oft we are curious in how long it will take on to pile up money or how provident we'd need to extend a loan to bring payments down to a reasonable level.

Examples

If you invest $2000 at 6% compounded every month, how long will it take the describe to double in value?

Get additional direction for this representative in the following:

How Much Money Has Congress Given For The Wall

Source: https://courses.lumenlearning.com/wmopen-mathforliberalarts/chapter/introduction-how-interest-is-calculated/

Posted by: chamblisswaregs.blogspot.com

0 Response to "How Much Money Has Congress Given For The Wall"

Post a Comment